Diesel-9

Well-known member

- Joined

- May 1, 2005

- Posts

- 527

"ON A LONG ENOUGH TIMELINE, THE SURVIVAL RATE FOR EVERYONE DROPS TO ZERO"

Sunday, January 18, 2009

Death Watch: Is Southwest (LUV) in Much More Trouble Than Perceived? Few More Words on Contango

We like Southwest - cheap tickets, drunk passengers on the Vegas flights, hot passengers on others, sweet equity ticker... Yet something is fishy in the city of Dallas... The company which was a perennial LBO candidate back in late 2006 and early 2007, somehow managed to escape unscathed through the "oil at $140" phase when most other airlines' shares had fallen to penny-stock levels. This can be attributed to its fortuitous hedging program that was started a decade ago, when its legacy competitors were trying to deal with outsized pension costs and massive debtloads (and most ended up in bankruptcy).

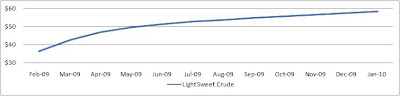

Now with oil crashing and contango getting steeper, it is curious how companies that hedged for the inverse are faring. In fact, one of the reasons cited by analysts for the deep contango is the unwind of the costless collars that companies such as LUV and JetBlue have had to do in past months. Southwest partially confirms this in its December 23 8-K filing where it notes it has drastically reduced its future hedging program by selling it zero-cost collars. The net market impact of this unwind is the forced selling of the near contracts (February 2009) and the purchase of far contracts. As the traded volume of near maturities is usually lower than that of the outer, the effect is a pronounced steepening of the near curve as seen below. If anyone is a NYMEX trader and can confirm or deny this we would love your feedback.

So what is the actual economic impact on heretofore beneficiaries of extensive hedging? Let's take the example of Southwest.

As the company was a heavy user of "zero-cost collars and fixed-priced swaps", it was benefiting while oil was priced higher than the average strike price on its derivatives which had been $75/barrel for the 2009-2012 period. In its July 24 Q2 results announcement and market update, LUV noted the "Fair Market Value of its hedges was $4.3 billion." At the time WTI was $125/barrel. It has now fallen to $36. Intuitively, FMV must have dropped dramatically, if not gone negative. As we are not specialists in fudging whatever FASB rule is responsible for determining FMV of Derivative contracts we will ignore this for now and instead focus on its most direct corporate proxy - cash. Here are the facts:

Sunday, January 18, 2009

Death Watch: Is Southwest (LUV) in Much More Trouble Than Perceived? Few More Words on Contango

We like Southwest - cheap tickets, drunk passengers on the Vegas flights, hot passengers on others, sweet equity ticker... Yet something is fishy in the city of Dallas... The company which was a perennial LBO candidate back in late 2006 and early 2007, somehow managed to escape unscathed through the "oil at $140" phase when most other airlines' shares had fallen to penny-stock levels. This can be attributed to its fortuitous hedging program that was started a decade ago, when its legacy competitors were trying to deal with outsized pension costs and massive debtloads (and most ended up in bankruptcy).

Now with oil crashing and contango getting steeper, it is curious how companies that hedged for the inverse are faring. In fact, one of the reasons cited by analysts for the deep contango is the unwind of the costless collars that companies such as LUV and JetBlue have had to do in past months. Southwest partially confirms this in its December 23 8-K filing where it notes it has drastically reduced its future hedging program by selling it zero-cost collars. The net market impact of this unwind is the forced selling of the near contracts (February 2009) and the purchase of far contracts. As the traded volume of near maturities is usually lower than that of the outer, the effect is a pronounced steepening of the near curve as seen below. If anyone is a NYMEX trader and can confirm or deny this we would love your feedback.

So what is the actual economic impact on heretofore beneficiaries of extensive hedging? Let's take the example of Southwest.

As the company was a heavy user of "zero-cost collars and fixed-priced swaps", it was benefiting while oil was priced higher than the average strike price on its derivatives which had been $75/barrel for the 2009-2012 period. In its July 24 Q2 results announcement and market update, LUV noted the "Fair Market Value of its hedges was $4.3 billion." At the time WTI was $125/barrel. It has now fallen to $36. Intuitively, FMV must have dropped dramatically, if not gone negative. As we are not specialists in fudging whatever FASB rule is responsible for determining FMV of Derivative contracts we will ignore this for now and instead focus on its most direct corporate proxy - cash. Here are the facts:

- At September 30 the company noted it had $2.4 billion in cash equivalents and $2.5 billion in Fair Value of fuel derivatives, already a big drop from the $4.7 billion in cash and $4.3 billion in derivatives 2 months prior (WTI was at $100 on Sept. 30). Also the company decided to access $400 million of the $600 million available under its revolver in October, so the net cash balance would have been roughly $3.0 billion around that time, excluding the FV of fuel derivatives.

- On a December 23 update the cash balance had dropped to $1.3 billion, net of $250 million in cash collateral calls, a huge drop from 2 months prior. One could say the FMV at this point is negative: over $4 billion in "value" lost from June 30, and $3.5 billion in cash equivalents burned in less than six months for a company which is otherwise supposed to be free cash flow positive!

- On the same update, the company announces it has essentially offset/sold its derivatives and only hedges 10% of its 2009-2013 fuel costs.

- Allegedly, the "modification of the hedge portfolio has significantly reduced the Company's current exposure to cash collateral requirements."

- Nonetheless, at the same time LUV is feverishly raising cash: the day before the Dec. 23 update it sells $400 million 10.5% Notes due 12/2011 which are secured by 12 737-400 aircraft; On Dec. 23 it announces it is pursuing a $350 million sale-leaseback of 10 737-700 planes at an interest rate of roughly 9%, the leaseback is completed on Jan 8. Also curiously, an amendment (8.01.b) to its fuel hedge agreement on Dec. 23 stipulates that until January 2010, LUV has to continue to post cash collateral if "the obligation is below $300 million or over $700", but if it is inbetween the company has agreed to "pledge 20 737-700s in lieu of cash"... quite odd, yet we wouldn't be surprised if this is exactly what happens.

- If the company's claim that its hedges are truly no longer a drain of cash, then its cash balance on the January 22 earnings call should be about $2 billion ($1.3 billion + $750 million new proceeds), all else equal.

- Furthermore, the company has a cash collateral rating trigger: if its credit rating (Baa1/BBB+ currently) drops below investment grade, it would have to post cash collateral with many more counterparties. This would imply a three notch downgrade. While S&P, in a recent omnibus report claims it is not likely to downgrade LUV soon, a significant downside surprise on January 22, or additional debt-capital raises could easily change analyst Betsy Snyder's opinion.

- The continuing contango steepening is indicative that someone keeps on unwinding costless collars: is it JetBlue, Delta, or is Southwest continuing to deleverage its bad future exposure all the while having to post cash collateral?

- Aside from just meeting its ongoing cash needs, Southwest is faced with a cliff of future contractual obligations. Its current fleet of 520 737s (425 owned, 95 leased as of the 10-K filing) is due for modernization, with 200 aircraft approaching retirement age at 16.7 avg. years (mostly 737 -300s and -500s). Its replacement plan consists of firm contracts and options to purchase up to 246 737-700s from Boeing; assuming it scraps its options, it still is on the hook to buy 108 airplanes over the next 5 years at a cost of $3.2 billion.

- And what happens if the company manages to unhedge successfully only to see a dramatic increase in the cost of crude? Goldman Sachs research currently expects LUV's 2009 fuel expense to be $2.1 billion based on 1,459 mm mainline gallons at $1.47/gallon or $62/barrel. If hypothetically oil were to go up to $90, the impact on LUV's EBIT and EBITDA, left naked without any hedges, would be -$1 billion (in other words each $1 change in oil cost is about $35MM in EBIT). And if oil is, again hypothetically, $90/barrel, there goes the company's projected $1 billion in 2009 EBIT.

Last edited:

")